What is the value of a financial advisor? The personal touch. Here are four stories of how flesh-and-blood advisors you meet in person (that’s opposed to a robo-advisor, where your contact is digital or over a phone line) benefited their clients.

These good advisors helped clients to overcome emotionally based decisions, stop them from making mistakes, figure out whether to make a big purchase and decipher arcane retirement plans. We’ll have separate articles throughout the summer describing in greater detail how they helped their clients.

Planning is so very vital for your future. According to a study by insurer Northwestern Mutual, a large majority (72%) of U.S. adults believes that the economy will suffer future crises. But two-thirds of them don’t have a financial plan. Plans are not static. Once you have a plan in hand, ongoing contact with your advisor is vital to make the plan work.

In our four cases, the advisor:

Prevented an emotional decision. A client of Nicholas Atkeson and Andrew Houghton, the founding partners of Delta Investment Management in San Francisco, feared that the stock market was getting too frothy recently and it was time to sell. No one can predict the market, and the wisest course is to have a well-diversified portfolio that you stay true to through good and bad times. There is room for rebalancing, certainly, but panicked decisions are almost always bad ones.

“Our role as financial advisors is to gently guide the client back on the road to smart portfolio management,” Atkeson and Houghton write. “The best deed we have done for a client is simply telling him it is a bad idea to be ruled by emotions.” The client relented from this ill-chosen decision.

Headed off an investment mistake. It’s amazing how often you come across seemingly great investment opportunities. Guess what? They are traps. Karl Schwartz, an advisor with Hewins Financial Advisors in Miami, notes that a client knew “a guy” who could get him into a sure-fire money-making investment, a South African gold mine. Trouble is, there is no such thing as a sure-fire investment. Schwartz managed to convince his client, through patient persuasion, that this great plan simply was not a good one.

When you hear about such bonanzas, Schwartz reports, “you cringe, as you know right away it’s a bad idea for the client.” Gold did well after the financial crisis but has lagged lately. It defines volatile.

Helped make a big purchasing decision. The question of whether to buy or rent is a major item in people’s lives. For many, their home is their largest asset. John C. Fales, lead advisor Allos Investment Advisors, which has offices in Phoenix and Overland Park, Kan., had a client who inherited some money and wanted to know how best to deploy it. He could buy a home for $150,000, or over the next 25 years, could pay out $300,000 in rent.

Fales did the math and figured out that, in this instance, it made more sense to buy. The client likely would have money left over to put into other investments, which would not be so if he were shelling out for rent over the next quarter-century.

Decoded abstruse pension details. A knotty problem confronted a client of Adam D. Koos, founder and president of Libertas Wealth Management Group, in Columbus Ohio. The client, a fireman, had previously been a police officer for eight years. When he quit the force, he collected his pension money as a lump sum. Now in his 50s, he wondered if he could buy back those eight years and thus boost his pension in the state-run pension fund for cops and firefighters.

Koos crunched the numbers and discovered that, for $80,000, the client could buy back the lost time and end up with a pension worth $500,000. As Koos puts it, this gives his client the “confidence that he and his wife will be able to retire on time and spend their later years doing what they enjoy.”

This person-to-person advice is invaluable.

Jobs are plenty, the stock market is hot, and the economy is firing on all cylinders. It won’t always be like that. Find out if you’re prepared for any type of market with a FREE PORTFOLIO CONSULTATION. We can also help with big purchasing decisions like buying vs renting or knowing when to take social security distributions.

For today’s younger couples, taking a drive along the winding road of finances is a lot different than it used to be. There are so many choices—each one steering the young couple closer or further away from the dreams of a lifetime. Hanging in the balance are two individuals hoping that their decisions will be in their overall best interest.

To better understand some of the challenges facing young families, meet Raj and Priya Chopra. They’re both in their late twenties and were married three years ago. Priya is a registered nurse and Raj is a marketing representative for a medium-sized technology company. Up until this point, they’ve enjoyed a lifestyle supported by two incomes. Without children, they’ve been able to be somewhat carefree about their spending.

Now, however, they are contemplating buying a home and having children. This has certainly raised questions about the financial implications of enlarging their family, as well as their financial future. Although the Chopras’ jobs seem relatively secure, they have friends who work for companies that have experienced significant downsizing and who are less certain about their future employment situation. Moreover, some of their friends have lost jobs and are going through difficult transitions.

Discussions with family and friends have led them to the conclusion that uncertainty may be the defining characteristic of their generation. Emerging families like the Chopra’s are facing a new reality, one with much more uncertainty about the future than that faced by previous generations. Some of this uncertainty is tied to rapid technological changes and some is the result of the realization that they personally may be responsible for providing for themselves much of what was previously provided by others (e.g., pensions by employers; social programs by the government).

There are many issues facing Raj and Priya, and they’ll need to ask themselves some difficult questions such as: Will corporate downsizing eventually catch up to them? If Priya intends to return to work full-time after having a baby, how would they cope if one of them should lose their job? What about the world of work in general? Will they go through several career transitions over the course of their working lives due to an economy that might be changing constantly? Is there a way to protect themselves financially? How difficult will it be for them to save for a child’s education? What about saving for more than one child? They both participate in 401(k) plans at work, but will they be able to save enough for a comfortable retirement? What about Social Security? Will the system change significantly? Will they be protected should they become sick or disabled?

What can a young couple like Raj and Priya do? A good first step is to discuss the various alternative solutions to these difficult questions. By doing so, Raj and Priya will be able to arrive at a realistic assessment of what they should and should not do financially, what they can and cannot afford, and what sacrifices they might need to make to assure financial security for both today and tomorrow. They know that their spending choices will have to be made carefully, and that preparing for a bright financial future will require setting goals now.

As the Chopra’s continue down the road of finances and look to expand their family, they can be a bit more optimistic about their future. The financial decisions they make today will make them less likely to be caught off guard by sudden economic or personal “bump in the road” tomorrow.

Is your 401k optimized to help you meet your retirement goals? Want to learn how to save thousands in taxes by making tax efficient invstments? Is your family covered if something were to happen to you or your spouse? Need help making these decisions? Talk to an advisor with your best interest in mind.

This question has frequently popped up in my first year as a Financial Advisor. It’s a good and fair question, albeit a loaded one. When I hear that question, I believe most people are referring to investing. If so, the answer is not sexy or surprising – it’s long-term, buy and hold. However, good financial advising is about more than just investing. Real financial advisors look at a client’s entire picture. They take debt, college planning, real estate, insurance, and estate planning into account. However, even here, the answers across planners are pretty standard:

Save more than you spend

Pay higher interest debt first

Invest in a 529 plan

Term life insurance is usually better than whole life

Have a will and a living trust

Nothing shocking. Execution is often more difficult than the theory but it’s pretty straightforward. Now, you may be asking, “what makes you so special?”

For one — I’m tall, brown, and handsome. Hopefully, that’s enough to gain your confidence but if not, I do have a couple financial philosophies that differ from most advisors.

Enjoy your latte and avocado toast

There’s a recent article in Money Magazine titled, Millionaire to Millennials: Stop Buying Avocado Toast If You Want to Buy a Home.

I mean…really? In that article, an Australian property mogul insinuated that folks shouldn’t eat out so much or buy a $4 cup of coffee if they want to afford a house. Well, doing some quick back of the envelope math, sacrificing a latte a day would mean that you would have enough to afford a down payment in San Francisco by May of 2195. That’s 65,000 lattes.

The Money Magazine article reminded me of a story I once heard from Morgan Housel, a Loeb Award finalist for financial journalism. It’s about a guy taking a smoke break with his non-smoking colleague.

“How long have you been smoking for?” the colleague asks.

“Thirty years,” says the smoker.

“Thirty years!” marvels the co-worker. “That costs so much money. At a pack a day, you’re spending $1,900 a year. Had you instead invested that money at an 8% return for the last 30 years, you’d have $250,000 in the bank today. That’s enough to buy a Ferrari.”

The smoker looked puzzled. “Do you smoke?” he asked his co-worker.

“No.”

“So where is your Ferrari?

If you don’t smoke you can substitute coffee for cigarettes and work through similar math. It’s the type of math many advisors use when speaking to colleagues about saving every last buck and letting the magic of compounding interest do its work. However, it doesn’t take into account the simple joys in life. Sure, not buying a pack of cigarettes or a Starbucks a day will save you money. But it may not save you from strangling your boss. Within reason, vices can be good for people; there’s an upside to happiness.

The goal of financial advising should not be to put a stop to happiness but to help you find ways to achieve the life you want. That probably involves a few vices or experiences that just feel good.

The market can be beat

Studies have shown that over a 10 year period, more than 85% of fund managers failed to perform better than the S&P 500. These statistics have led many advisors and those in academia to conclude that the market cannot be beaten.

I don’t buy into what academia attempts to preach. Imagine if a medical student was told that no matter how hard they try; they will just be a mediocre doctor. Investing and portfolio management is probably the only subject matter where professors will tell their students that it’s impossible to be better than average.

All the statistics tell me is that mutual fund managers cannot beat the market. I believe individual investors can.

Mutual funds have a tougher battle than individual investors. Fund companies have to hire portfolio managers, research analysts, compliance folks, sales teams, and accountants. These people cost money and they are paid through the contributions from investors, therefore hindering investment returns.

There is also unbelievable pressure for those funds to outperform the market on an annual or even quarterly basis. Therefore, stocks are being bought and sold frequently, not giving a sound investment idea time to perform. Fund managers also face pressure from their bosses to go with the herd. A couple years ago, every manager was all-in on Apple stock. However, when signs of slowing growth started to emerge at Apple, the stock declined nearly 30% from its highs. Many of the funds that were overweight in Apple struggled. However, those managers weren’t going to lose their jobs because, “hey, it’s not my fault — everyone was invested in Apple.” Had the stock gone up 30% and a manager was not invested in the popular company, they may be on the hot seat. Of course, Apple recovered but the point is that it’s tough for fund managers to go against the grain. As an individual investor, you do not face that same pressure.

You as an individual investor can avoid Wall Street’s outrageous fees and short-term pressures. Your edge is that you have the advantage of time. Your investments don’t have to be better than the competition every year or quarter. You can own great companies and give them time to run.

Now, don’t get me wrong. I’m not saying that beating the market is what you should be trying to do. As an individual investor, you should try to do well enough to achieve certain goals such as retirement or paying for your children’s college education. This can often be done by just investing in a diversified mix of low-cost index funds. This alone will likely lead to better returns than 85% of mutual funds. However, investing in high-quality individual stocks alongside those index funds can be a great way to enhance returns.

Is your 401k optimized to help you meet your retirement goals? Are you paying too much in fees for under-performing funds in your retirement plan? A 14-year Vanguard study showed a good financial advisor can add up to a 3% value to its client — a difference of $500,000 for someone maximizing their 401k over 20 years. Click below to schedule an appointment for a FREE 401k evaluation.

The following snippet is from a CBS article written during the heart of the 2009 financial crisis.

Alan Weir, who turns 60 this month, showed 60 Minutes his latest 401(k) statement, which he hadn’t had the courage to open up.

“I’m afraid,” he told correspondent Steve Kroft.

There’s good reason for his trepidation: nearly half of his life savings have vanished in a matter of months.

“It went down again,” Weir told Kroft, after opening the statement.

Overall, he said he was down about $140,000.

Asked if he thought he’d ever get that money back, Weir said. “I probably never see it come back. I was looking to retire, probably, when I hit 62. Can’t do it now. I’ll probably be working until I’m at least 70.”

Stories like Alan’s were all too common in 2008 and 2009. Similar headlines were popular during the dot-com bust in 2001. With unemployment below 5% and markets at all-time highs, it’s easy to forget about delayed retirements, foreclosures, evictions, and long lines at local job fairs. As time passes as retirement accounts grow larger, it’s easy to forget the pain of past market crashes. However, investors may be seeing some signs that it’s time to be a little cautious. Are we in a bubble? My favorite financial writer is Morgan Housel, who in this article pointed out that the word “bubble” didn’t even exist in the financial dictionary 25 years ago. With the bursting of the technology and real estate bubble fresh on our minds, that word is now thrown around frequently. Housel mentions that today, according to the media, we are in at least 14 different bubbles:

• A new real estate bubble. • A bond bubble. • A tech bubble. • A VC bubble. • A startup bubble. • A stock bubble. • A shale oil bubble. • A healthcare bubble. • A dollar bubble. • A college tuition bubble. • A Canadian housing bubble. • A central bank bubble. • A social media bubble. • A China bubble.

The word bubble makes for a great headline that gets clicks but are we really in a bubble today? When I look at the tech and housing bubbles, there are two similarities that stick out to me: 1) Valuations, measured by a variety of metrics, far exceeded historical averages, and 2) A clear majority of people thought that things were going to get better forever. Let’s look at how those 2 dynamics are playing out today.

The data One of my favorite metrics too look at when evaluating market valuation is the TMC to GNP ratio. This ratio measures the total value of all publicly traded equities (Total Market Capitalization or TMC), against the size of the entire U.S. economy (Gross National Product or GNP). The TMC to GNP ratio is often called the Buffett Indicator as billionaire investor Warren Buffett once called it “the best single measure of where valuations stand at any given moment.” He goes on to say, “If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you. If the ratio approaches 200%–as it did in 1999 and a part of 2000–you are playing with fire”. Today, TMC/GDP ratio sits at 130.8%, a level only surpassed during the tech bubble.

Source: Gurufocus.com

Another popular valuation metric is the CAPE Ratio, created by Robert Schiller, a Yale professor and American Nobel Laureate. The CAPE ratio, or cyclically adjusted price-to-earnings ratio, takes a popular valuation metric, the P/E ratio and expands it by adjusting for business cycles and inflation. The CAPE ratio is not an indicator of upcoming market crashes. Schiller’s research concludes it is an indicator of future long-term market returns.

Yet, at a ratio of 29.5, the only two times the CAPE ratio was higher than today’s level was leading up to the Great Depression and the dot-com bust.

Source: Gurufocus.com

Although the CAPE ratio appears to be at dangerously high levels, investors should be aware of a strong argument against this metric. The long-term average of 16.7 is deceiving as the denominator used to calculate the CAPE ratio, earnings, is skewed downwards as more profitable technology companies replaced lower margin industries which dominated the S&P 500 in the past. Furthermore, earnings can not only be manipulated but can vary through time as accounting rules change. Despite its flaws, the CAPE ratio is still one of the strongest indicators out there used to predict future market returns.

The emotions When I first started investing about 15 years ago, I merely focused on the numbers. The dominant left-side of my brain gravitated towards financial statements and economic data. However, as I gained more experience, I realized that understanding human behavior was just as important as understanding data when trying to gauge the markets.

So, what is the pulse of today’s bull market? In a recent Bloomberg View podcast, legendary investor Howard Marks noted three stages to a bull market:

1. A few bright people believe there could be improvement 2. Most people believe things are getting better 3. Every idiot thinks things are going to get better forever

In hindsight, it’s easy to state that the housing and tech bubbles were discernable. How easily people forget. Middle managers quitting their full-time jobs to become day traders was a recurring theme in the late 90’s. Move forward a decade and all the talk was about how “they aren’t making any more land.” Both time periods were filled with irrational exuberance as the road to riches appeared to be as easy as buying a few tech stocks or five townhomes in the Arizona desert with no income verification.

I don’t see this type of euphoria today. In fact, the market rally of the past seven years might be the most hated rally in the history of markets. The S&P 500 is up over 230% since reaching its lows in March 2009. Yet the commentary during that entire time has been that markets are overvalued, the Fed is incompetent, Wall Street is rigged, and Bitcoin will rule the day. Additionally, the political divide is larger in the U.S. than it has ever been. The national debt is still at high levels. Interest rates have been at or near zero for nearly a decade. But rather than ignoring these facts, there appears to be general concern with those that pay attention to this kind of stuff.

Although the data shows stretched valuations, the euphoria that exists during bubbles is not as prevalent as it has been in the past. This doesn’t mean there won’t be a correction. In fact, there will be. There always has been. It’s a part the cycle.

The S&P 500 has fallen 10% or more from recent highs a total of 46 times since 1929, an average of about once every couple of years. The definition of a bear market is a drop of 20%. The S&P 500 has experienced a bear market over 20 times, or once every four years. We last saw a 10% drop in January 2016, which is about on schedule. The last time there was a 20% drop was nearly 6 years ago (it was a 19.4% drop but let’s call it a wash).

It’s a matter of time before we see another bear market. We’re due. However, that doesn’t mean it will happen soon. Although markets appear to be overvalued, nobody has been able to predict downturns and it’s no different this time. Therefore, pulling your money out of the market completely could mean you can lose a lot of money.

So what should you do?

You hear this term diversify all the time but what does this word really mean? Of course, you don’t want all your money in Groupon stock but is investing in a S&P 500 index fund diversified enough too? Many investors investing in the S&P 500 gets broad market coverage at a low cost but the problem is that your portfolio will only be in the largest U.S. companies. It ignores the rest of the investment universe, not only across the U.S., but across the globe.

What’s wrong with owning just the U.S. market? Sure, it’s comfortable. It’s like that warm and fuzzy blanket you wear when watching seven straight episodes of Narcos. However, the total market value of the U.S. stocks is only 43% of the global market. As a share of GDP, the U.S. is only 20% of the global share. Yet, according to Vanguard, U.S. investors have 72% of their portfolios in U.S. stocks.

If you had all your money in U.S. stocks since the market lows of March 2009, this concentration wouldn’t be a bad thing. The U.S. market has been much stronger than global markets since the Great Recession. However, this is not always going to be the case. Going forward, investors should expect much lower returns. Going back to the CAPE ratio, long-term returns with the CAPE ratio above 25 has only been about 1% when adjusting for inflation. Returns have been negative when they go above 30. Recall that the CAPE ratio is at 29.5 today.

A diversified portfolio means buying a variety of asset classes. An asset class can consist of investments in government bonds along with stocks of large, medium, and small companies. It will also include international stocks and bonds, real estate, and commodities. A diversified portfolio that invests in each of these asset classes won’t always get you returns as high as you would if you focused on a single asset class. However, there’s no way of knowing which asset class will outperform the others. If there was, I would still be blogging…it would just be from Belize.

The goal with diversification is not to outperform everyone else but to have a portfolio that will do well in multiple markets. It’s to keep you in the market when things go awry.

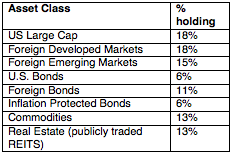

Let’s look at a diversified portfolio in action. In his book, Global Asset Allocation: A Survey of the World’s Top Asset Allocation Strategies, author Mark Faber looked at the returns and volatility of various asset strategies. One of the better performing strategies was that by former Harvard endowment chair Mohammad El-Erian. His portfolio strategy consisted of the following asset classes:

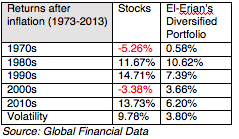

Below is how this diversified portfolio performed.

Notice how the diversified portfolio trailed stocks when they were going up. However, during bear markets, losses were protected. Additionally, volatility was significantly reduced. A diversified portfolio netted positive returns in a variety of investment environments while only having 25% of the volatility. This is important as investors will more likely not regretfully sell their entire portfolio in the event of an inevitable bear market.

Other strategies Money is emotional. Academic studies show that the best time to invest is always today rather than time the market and attempt to get in or out at the best moment. If we were all robots, this would be a great strategy. However, many people have been left with a sour taste in their mouth regarding Wall Street and that’s okay. Others are fearful of an overheated market and that makes reasonable too. If your worried about what the future holds, focus on the following:

1. Change the focus of your hard-earned dollars. A good start would be paying down some debt. It could also be a good time to get to that home remodel you’ve been putting off. Do you have enough of an emergency fund that can something unexpected occurs? Basically, use this time to evaluate your personal financial situation outside of the investment world.

2. Start hoarding cash. Rather than selling out of your investments which is one of the biggest mistakes individuals can make, just stop contributing for a little while. If you receive a tax benefit by investing in your 401k, you should still take advantage of it. Most plans give you the option to invest in cash or other low-risk investments. It’s no guarantee that the market grants you a buying opportunity, but if it does, you’ll be ready to make your cash work at a cheaper price.

3. Don’t change a thing. The number one factor in determining investment success is time. Going back 40 years, an investor could have only added to the market just before a big crash and they still would have made money if they held on during the rough patches. If you have years ahead of you and don’t need to tap your investment portfolio anytime soon, just keep investing what you can and ignore the market gyrations.

4. Know where you stand. Contrary to not changing a thing, if you are close to retirement and will be reliant on your investment portfolio, take a close look at your portfolio. Make sure you aren’t putting yourself at risk of becoming a 60 Minutes story. However, you also must be mindful of not getting too conservative and putting yourself at risk of running out of money during retirement. I know a good financial advisor who could run the numbers and assist in letting you know where you stand.

To be clear, I’m not making a market call on a stock market correction or bear market. The global markets are complex and nobody has been successful in finding a secret formula that predicts short-term movements. However, having a diversified portfolio and sticking with it during good times and bad has proven to be a winning strategy over the long-term.

Need help building that diversified portfolio or just want a 2nd opinion? Allow us to help you create a portfolio built for a bull or bear market. Get started today by clicking the link below for a FREE consultation.